EXCLUSIVE: Medibank sale clouded by 1977 documents

Declassified cabinet documents from 1977 obtained by The New Daily reveal that Fraser government ministers saw the Commonwealth’s role in the health fund akin to a creditor and supplier, rather than as an owner, and further cloud the Abbott government’s plans to sell the insurer.

Although a public authority — the Health Insurance Commission — managed Medibank Private, senior ministers were careful not to make any ownership claims over the fund’s assets on behalf of the Commonwealth either in public, or in secret cabinet meetings.

The 1977 cabinet minutes, obtained from the National Archives of Australia, are replete with evidence of the government’s non-proprietorial attitude towards the insurer.

They appear to support arguments made by policyholders that the federal government was never the owner of Medibank Private before controversial legislation introduced by the Howard government installed the Commonwealth as the sole shareholder in 1998 at a cost of only $100.

The 1977 documents raise more questions about the validity of that legislation and the ability of the Abbott government to sell the idea that its ownership of Medibank Private is incontestable.

The decision to launch Medibank Private in 1976 created a big organisational problem for the expanding Health Insurance Commission. By the end of the year it had 348 staff scattered in six separate buildings in Canberra.

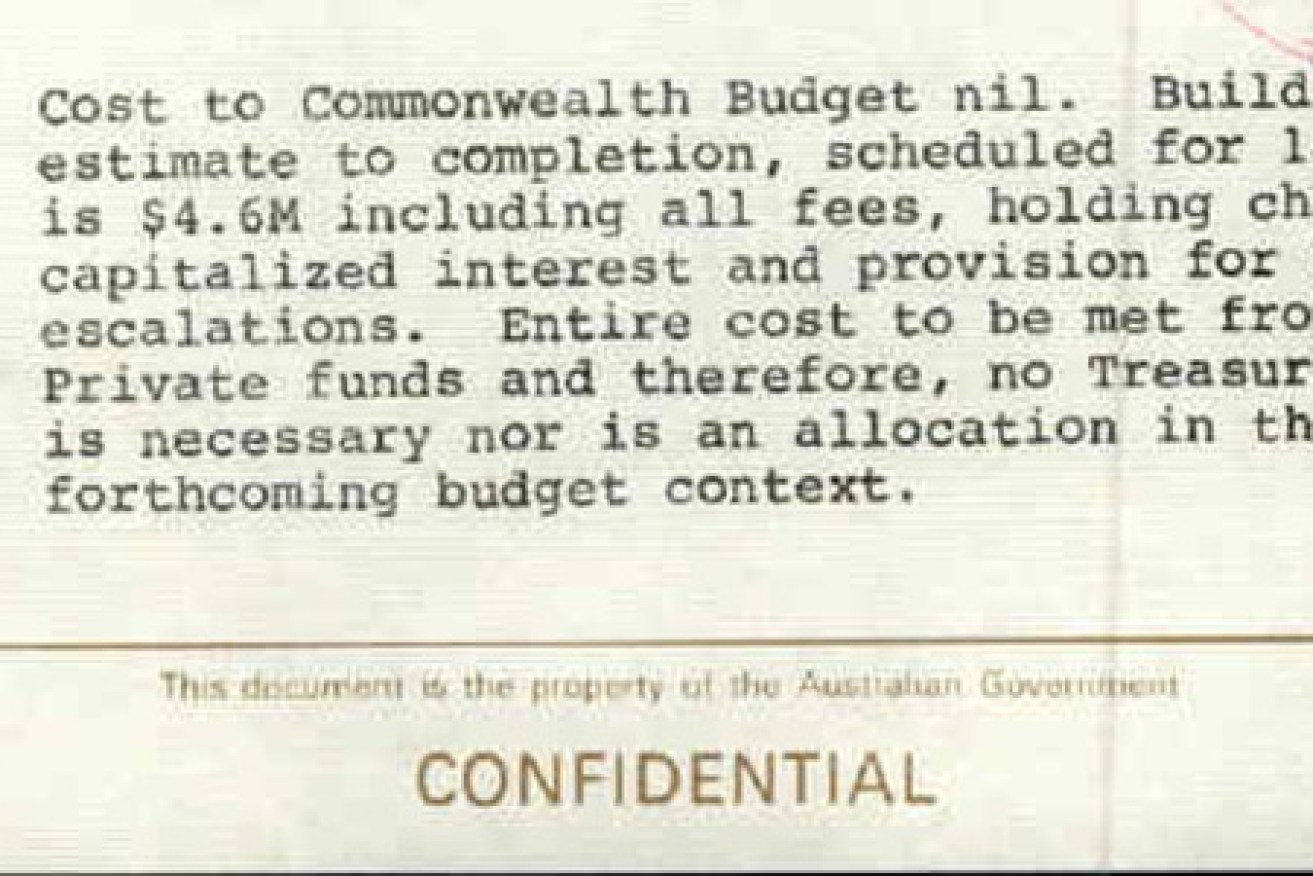

In early 1977, the commission drafted a proposal to build a new central office in the suburb of Woden using funds to be put up by taxpayers.

The Fraser government rejected this idea, but accepted another plan that involved financing the project with cash sitting on Medibank Private’s balance sheet.

According to statements made to cabinet by health minister Ralph Hunt on 20 June 1977, the cost of the project was “nil” from the Commonwealth’s perspective:

“Entire cost to be met from Medibank Private funds and therefore, no Treasury funding is necessary nor is an allocation in the forthcoming budget context.”

Under the proposal, which was later endorsed by finance minister Ian Viner, the Health Insurance Commission was able to start the project on the understanding that it would be able to lease the new building from Medibank Private.

It was a commercial transaction between the Health Insurance Commission and Medibank Private that recognised the assets of the health fund did not belong to the government.

On advice from the Attorney General’s Department, a private company — owned by Medibank Private — was set up to oversee the construction and the financing of the new facility.

The project cost an estimated $4.6 million and none of the capital came from the Commonwealth, according to the cabinet documents.

After the new office centre was built, the Health Insurance Commission negotiated a lease with Medibank Private under which it agreed to pay rent to the health fund. It later purchased the building from the health fund.

The structure of these transactions reflected understandings within government at the time that the assets of the health fund were distinct from those of the Commonwealth.

The 1977 cabinet documents also highlight another issue that confirms the Commonwealth’s non-proprietorial attitude towards Medibank Private.

In approving the HIC’s plan for developing the new offices, the Department of Finance in August 1977 requested the commission to commit to a timetable for repaying a $10 million “advance” made by the Commonwealth to help set up Medibank Private.

In fact, the government directed the HIC to identify $10 million of Medibank Private’s investment assets as security until the loan was repaid. The money was returned to the government in 1983.

This transaction provides a stark insight into how the government saw itself as a lender to Medibank Private.

Not an equity investor. Not an owner.

Two decades later, the Commonwealth changed its mind.

George Lekakis has been a finance journalist for 20 years, working at the Herald-Sun, the Australian Financial Review and Alan Kohler’s Eureka Report. He currently teaches investigative and business journalism at Monash University.