Scams leave $229m hole in Aussie pockets

ACCC

Falling interest rates may actually be pushing more Australians into the arms of lurking conmen, according to a new report by the consumer watchdog.

Losses to investment scams almost doubled in 2015, to $24.4 million, according to complaints received by the ACCC’s Scamwatch service.

In addition, data from the Australian Cybercrime Online Reporting Network (ACORN) show another $17 million in reported losses to investment scams.

• Banks may drop the nice guy act after the election

• Woolies, AusPost drop in consumer index trust

• Shorten sidesteps penalty rates

Investment scams overtook dating and romance scams as the category with the largest financial losses reported by Australians in 2015, the ACCC’s Targeting Scams Report reveals.

“There are many other scams which affect older members of the community but these two scams account for half of the money reported lost by over-55s in 2015,” ACCC Deputy Chair Delia Rickard said.

Aussies are estimated to have lost an overall $229 million in 2015 to various scams, according to the report.

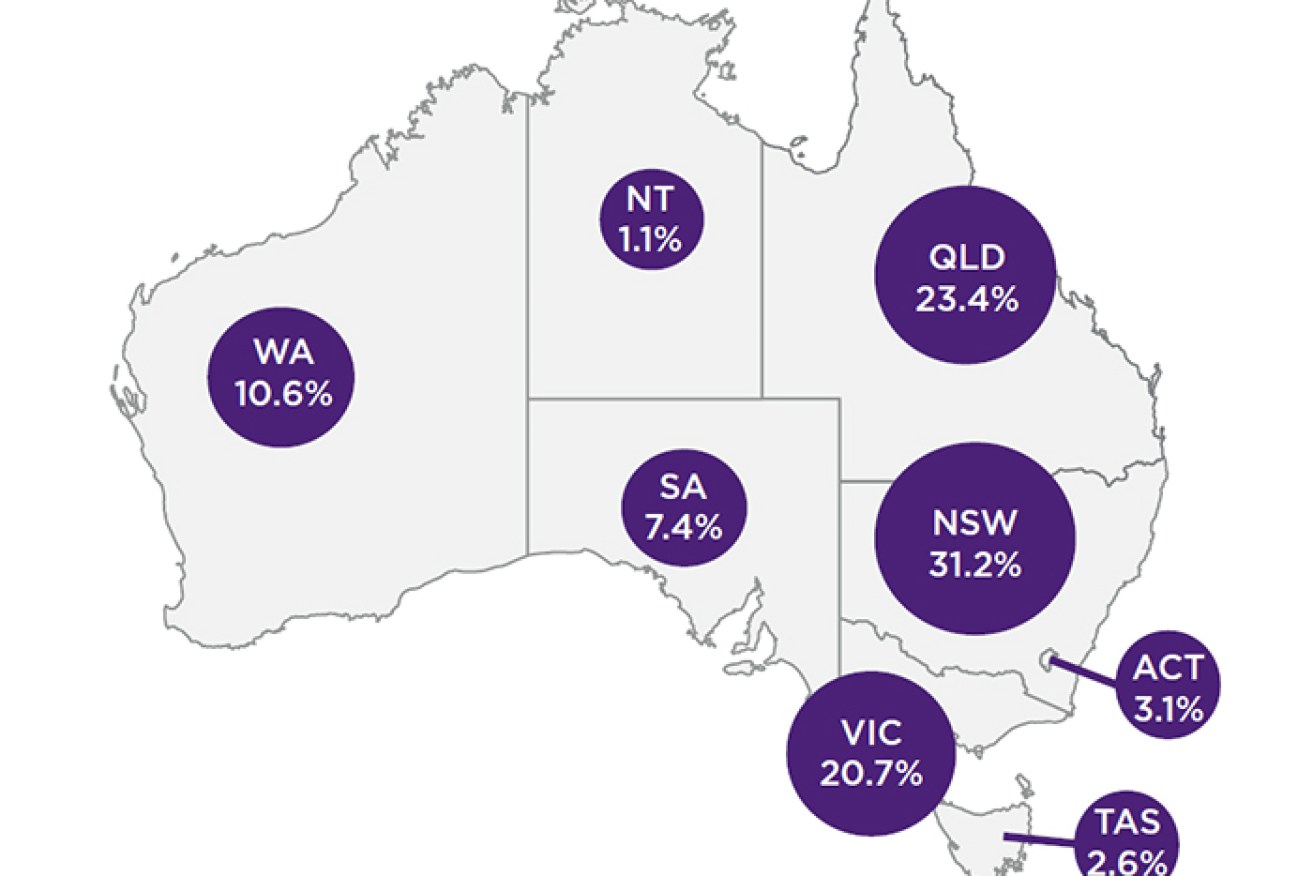

Scams reported in Australia by state in 2015. Photo: ACCC

The consumer watchdog’s Scamwatch service alone received 105,200 complaints, with $85 million reported lost.

Separate reporting to ACORN revealed losses of more than $127 million, detailed 25,600 complaints.

In addition, various scam disruption programs detected Australians sending funds to high-risk jurisdictions, with this unreported scam activity estimated to cost $17.1 million.

The Reserve Bank of Australia cut its cash rate twice in 2015 to a then record low of two per cent, then cut it again in early May to a new record low of 1.75 per cent.

Fraudulent investment scams posed a significant risk for Australians looking for investment opportunities, especially those looking to grow their retirement funds, the ACCC said.

The scams come in many guises including business ventures, superannuation schemes, managed funds and the sale or purchase of shares or property, with opportunities dressed up with professional looking brochures and websites, Ms Rickard said.

While phone scams remained the most common, 38 per cent of scam approaches occurred through email, over the internet or through a social network platform.

The regulator said education and community awareness remain key tools to combat scams and reaffirmed that its 2016 priority was to reduce the impact of scams through education and disruption.

-AAP

Woolworths faces court over $1m pay bungle

Spend some time to examine cashback details

Apps that help you save on fuel, groceries, time

Fridge, pantry audits vital to cut food waste

Aussies’ mortgage pain hits unwanted high

Jobs market put to test with fresh data due