Big banks abandon rural communities

Australian banks and building societies are continuing to abandon their face-to-face banking services, with Westpac and ANZ culling more branches in the last year across rural and remote parts of Australia.

Westpac has axed almost 150 in-store banking outlets in the past 12 months after negotiating a national agency deal with Australia Post.

• How predatory banks are hooking credit cards customers

• Banks milking customers on credit card rates

The latest cutbacks have provoked anger in rural towns, including Crookwell in the NSW Southern Tablelands, where Westpac customers were left without a face-to-face banking service after the bank terminated an agency arrangement with a local retailer in May.

Local councillors described Westpac’s decision as a setback for the town and are now trying to negotiate a deal with Bendigo Bank to enhance the banking services available in the town.

Regional players like Bendigo Bank have an opportunity to fill the gap left by the big four.

Westpac is reducing its retail banking footprint faster than any other local bank, according to official data published this week by the Australian Prudential Regulation Authority.

In very remote regions of the country, face-to-face banking is disappearing rapidly, with the number of bank and credit union outlets decreasing by more than 40 per cent since 2006.

While Australia Post continues to offer banking services to people in remote areas, the service is not available in all towns affected by bank closures.

Do we still need branches?

The boom in electronic platforms, including the internet, EFTPOS and automated phone services has rendered over-the-counter banking a thing of the past for millions of people.

However, consumer advocates believe that the latest cuts to rural banking services will marginalise low-income people in rural and remote areas.

Katherine Temple, the senior policy officer at the Consumer Action Law Centre, says the closure of banking services is still having marked impacts on country areas.

“We still think this is a big issue,” she said. “Closing branches and other services has the potential to deepen the digital divide because not all parts of Australia have reliable access to broadband.

“We want to see the banks do more to increase financial inclusion for low-income customers, rather than increasing the gap.”

A survey conducted by Anglicare Victoria appears to support Ms Temple’s concerns.

It found that only 51 per cent of low income families in Australia could afford home access to the internet.

A recent study of internet take-up by the Australian Communications and Media Authority found that 28 per cent of all people living in rural and remote areas had no direct access to broadband services in 2014.

These findings indicate that millions of Australians still need branches for basic banking.

Digital payments may be taking over, but cash is still used, and businesses need a bank to deposit that cash in.

Westpac defends its decision

The Westpac decision means that thousands of rural customers will have to rely on Australia Post outlets to deposit and withdraw cash from their accounts.

That, of course, won’t help customers shopping for a loan in places like Crookwell because Australia Post only provides basic transactional services.

Westpac’s customers in Crookwell who do not have internet access either need to organise a meeting with a mobile banker or drive 45 kilometres to their nearest branch at Goulburn.

Westpac spokesman David Lording defended the bank’s decision, saying that the group had also invested heavily in online channels to provide customers with access to lending managers over the internet.

“Technology is continuing to change the way people do their banking – we’re seeing an increase in the number of customers using electronic services,” he said.

“If you’re a farmer and want a loan you can talk to a business banker through video conferencing.”

Peter Strong, the chief executive of the Council of Small Business Australia, said banks should always ensure they create alternatives for customers when they reduce face-to-face services.

“Until people stop using cash altogether, there’s still going be a need for branches,” he said.

“For rural businesspeople, managing cash can be risky – you can take the money home or hide it in a special spot but eventually you’ve got to have somewhere safe to take it.”

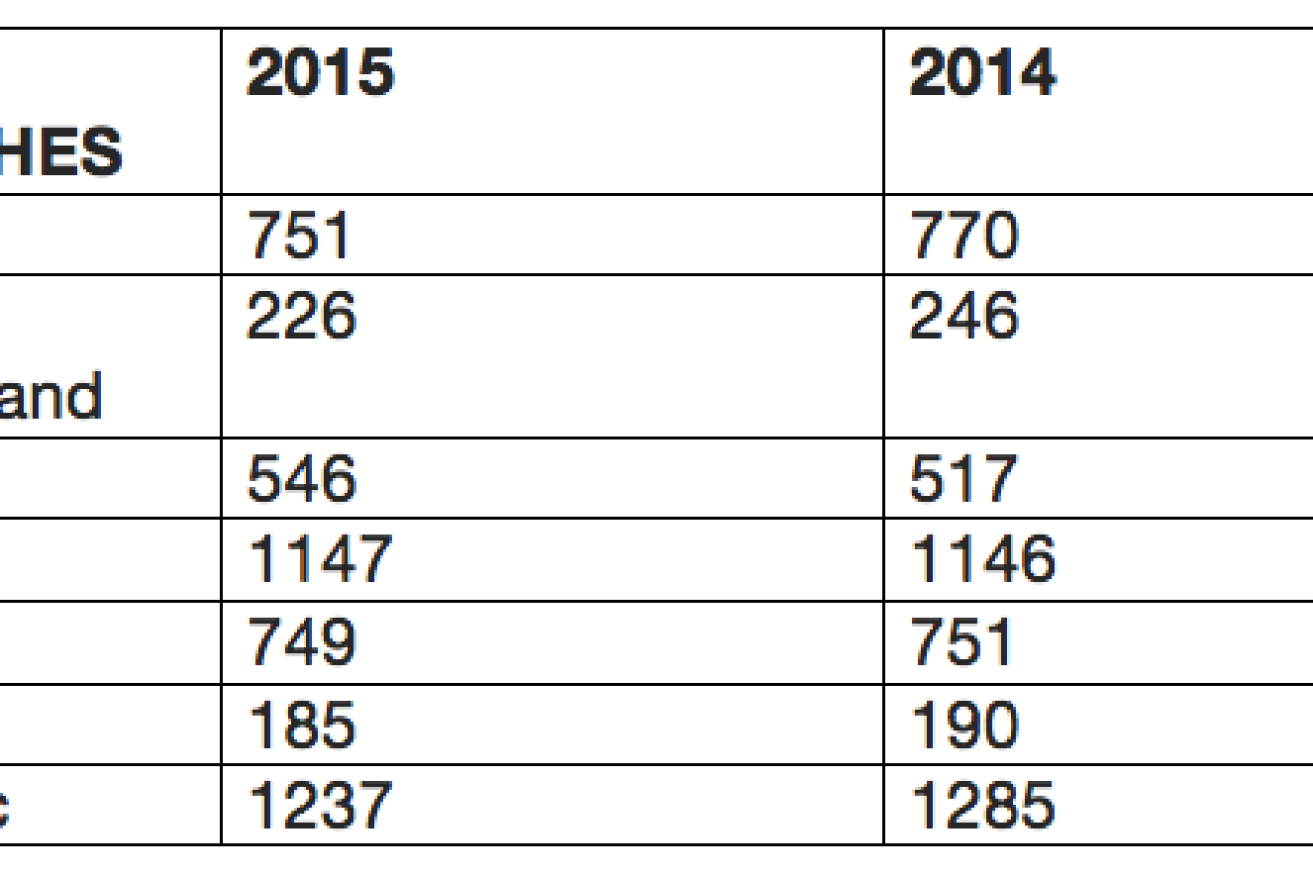

What the APRA data shows

Not all banks are reducing face-to-face banking services.

Bendigo Bank actually expanded its branch network by 29 to 546 outlets.

More than half of Bendigo’s branches are so-called “community banks”, in which members of local communities have committed capital to restore banking services in their towns.

At its current rate of growth, Bendigo’s network is likely to its overtake the branch representation of some of the major banks by 2020.

Woolworths faces court over $1m pay bungle

Spend some time to examine cashback details

Apps that help you save on fuel, groceries, time

Fridge, pantry audits vital to cut food waste

Aussies’ mortgage pain hits unwanted high

Jobs market put to test with fresh data due