Why there’s no money left in frontier Australia

Anyone who saw the recent ABC drama The Secret River will have a basic grasp of what economists call ‘extensive growth’ – the pushing back of frontiers and growth of a capitalist economy where none existed before.

In the two decades after the arrival of the First Fleet, Australia’s population increased tenfold as settlers and convicts poured off ships and set off to stake out their bit of the new economy.

Economic growth was highly dependent on the ‘extending’ of the economy, rather than making the businesses that made up the economy more ‘intensive’ – through greater capital-intensity and productivity.

• Visa, Mastercard making your shopping more expensive

• Rich executives want you to pay these taxes

• Why banks can’t justify ‘extortionate’ bank fees

What’s all that got to do with the Australian economy two centuries later?

A great deal, actually. As Melbourne University economic historian Ian McLean explained in his 2013 book Why Australia Prospered: The Shifting Sources of Economic Growth, extensive economic growth has been an unusually large part of the nation’s development right up to the present day.

Trouble is, two major sources of extensive growth are now reaching their limit.

Firstly, the mining boom has involved a protracted, and historically large inflow of capital from abroad. Building mines, processing facilities and transport routes costs a lot, and has employed a lot of Australians.

Mining firms have spent up big with mining-services firms. High-earning miners have been high-spending customers in retail businesses. And all of those transactions were recorded as ‘GDP growth’ during the boom years.

That boom is now well and truly over. Mining investment is contracting rapidly – the so-called ‘cap-ex cliff’, and the firms involved must enter an intensive development phase – better management, work practices and productivity.

The other big ‘extensive’ industry is more difficult to understand.

It’s the housing boom that began in the mid-1990s – a boom that has been underpinned by high levels of migration, as well as population growth via high-ish birth rates and oldies living longer than forecasters expected a couple of decades ago.

In fact, population growth has been large enough to dilute what otherwise looks like healthy economic growth.

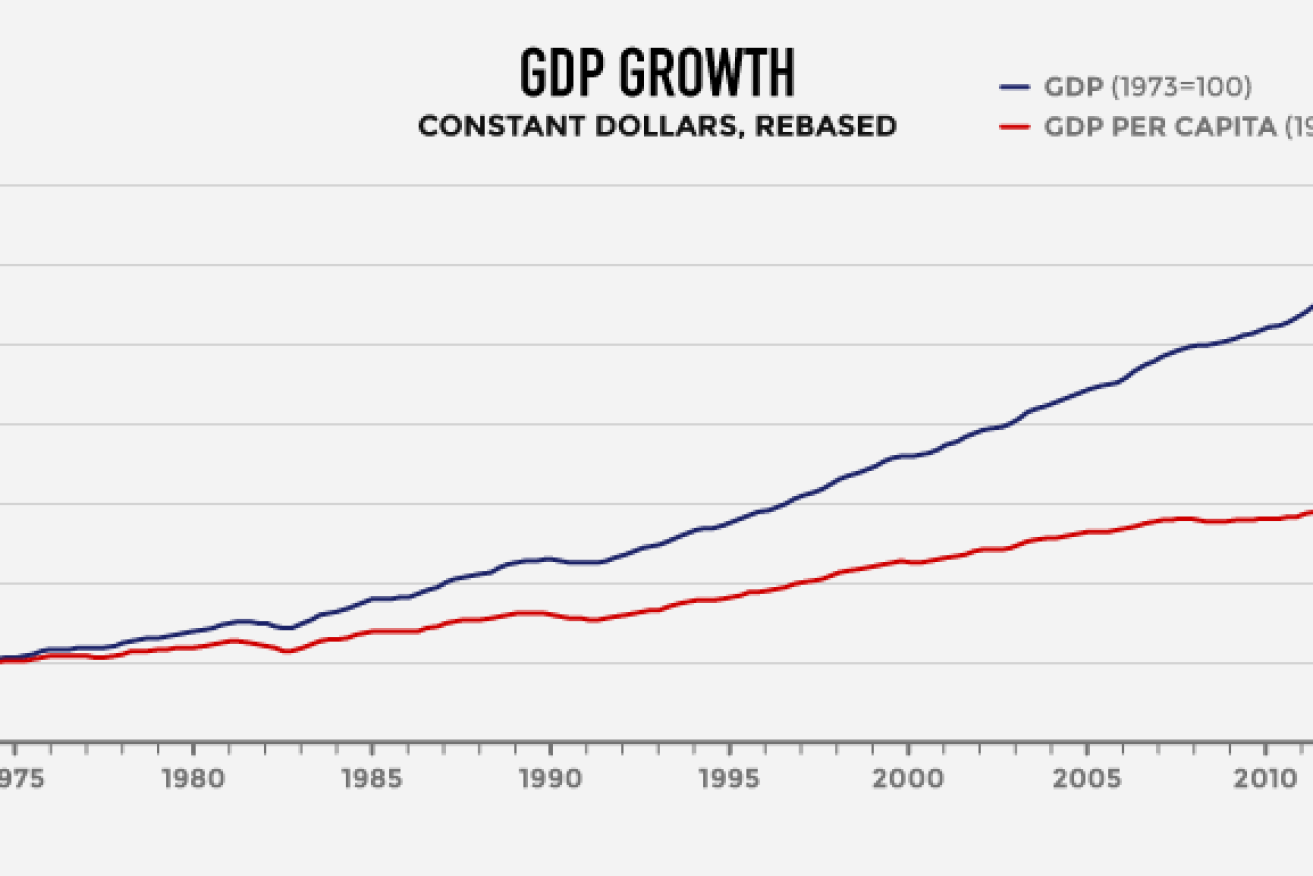

The chart below shows how GDP, and GDP per person, have diverged since the ABS began keeping accurate records for both in the early 1970s.

The top line represents the kind of growth figure Treasurers like to announce on budget day.

The top line represents the kind of growth figure Treasurers like to announce on budget day.

However, when corrected for population growth it looks much less impressive – the top line represents a compounding growth rate of about 3.1 per cent, but the growth per person rate was around 1.7 per cent.

The bottom line is not a bad proxy for tracking ‘intensive’ growth – it’s how much richer we got per person (about twice as rich over those years) rather than how big we grew by increasing the number of persons (about 3.5 times larger).

The ‘extensive growth’ attributable to the housing boom has to be more carefully picked apart than mining, because to economists not all of it counts.

The buying and selling of established homes doesn’t add to GDP.

As economist Bill Mitchell explained to me this week, the buying and selling of ‘second-hand’ goods, such as established homes, doesn’t add to GDP – though the incomes earned by banks, real estate agents, conveyancers and tradies renovating home for re-sale certainly do.

For two decades, capital has flowed from wholesale money markets into the Australian mortgage market, allowing homes to be mortgaged and re-mortgaged at successively higher values – none of which counts as ‘growth’ in itself.

However, the wealth effect of the large capital gains in the housing market has boosted GDP.

In the pre-GFC era, many home owners boosted their incomes by withdrawing equity from their ever-more valuable homes and spending it on consumption.

During the GFC years, while some Aussies deleveraged and the savings rate rose, consumption stayed fairly healthy because of government stimulus spending, intervention in housing (first homebuyer grants), and China’s stimulus spending on our resources exports. There was no house price crash here – and that kept consumers pretty chipper.

The residential construction boom of the past few years is also related, indirectly, to the run-up in property prices.

Apartment construction booms have boosted economic growth, as investors tried to get on the capital-gains bandwagon – and new dwellings count towards measures of GDP, unlike established homes.

But just as with the mining investment boom, the housing/population boom must come to an end.

In theory, today’s sky-high property prices could be maintained by allowing even higher levels of migration, to artificially increase demand for existing homes.

Industries such as tourism are slowly recovering after the boom years.

However, while this worked under the Howard, Rudd and Gillard governments, it won’t work now.

We no longer have the labour shortage we had during the mining boom years.

Nor are we, at present, an attractive destination for the large flows of global capital needed to create jobs for hundreds of thousands of migrants.

The extensive growth of the ‘houses and holes’ economy, therefore, is coming to an end.

What will replace those bounteous years?

Well, the first point to make is that more of the profits and tax revenues of those years should have been invested in raising productivity – through education, R&D, developing new intellectual property and so on – and investing in productive capital.

Because we spent so much of those extensive growth booms on consumption, Australia is now in the very difficult situation of having to invest, during hard times, to grow businesses that were stunted by the boom years.

Tourism, education exports, food processing, advanced manufacturing (remember the auto industry?) and so on were all hit hard by the high dollar during the boom years.

Now, they are staggering back to their feet (all except auto) and it will be a long, hard road to get them up to speed again.

Intensive growth, then, will be much harder to find than the low-hanging fruit of the extensive growth years.

And for the first time in decades, politicians who think they can revive the old model by ‘turning on the immigration tap’ are deluded – not that that will stop them trying.

Woodside shareholders reject climate plan

SA tops states’ economic leaderboard again

Woolworths faces court over $1m pay bungle

Spend some time to examine cashback details

Apps that help you save on fuel, groceries, time

Fridge, pantry audits vital to cut food waste