How Australia is caught in a China feedback loop

There has been a contradiction at the heart of Australia’s economic success in the past 15 years – capitalist Australia has been heavily dependent on state-capitalist China for its economic growth.

China’s state-owned enterprises, and their various free market joint ventures, have helped the Middle Kingdom achieve astonishing growth rates over those years.

A very large part of those growth rates came from construction and infrastructure work, for which massive volumes of Australian resources were needed.

• Asian markets in freefall after China’s massive losses

• Iron ore dives to six year low

• Peter Costello is wrong. You can trust super

The Chinese fixed-investment boom caused the prices paid for commodities such as iron ore, coal and copper to surge, and the profits and tax revenue that generated trickled down through the rest of our economy.

According to research by the Reserve Bank last year, that made us approximately 13 per cent better off than we’d otherwise have been if the mining boom didn’t happen.

The chart below shows this income effect. The top line represents how much richer we were on average, compared with the RBA’s best estimate of the ‘counterfactual’ of no mining boom at all.

That boost to wealth was a combination of increased economic activity (the volume effect) and the increased spending power of a higher terms-of-trade and therefore higher dollar (the trade effect).

Chinese investment caused the price of commodities to surge. Photo: AAP

What was rarely said during the boom, however, is that very few economists ever accepted that a state-directed economy could achieve the best allocation of resources, and therefore the best growth rates, in the longer term.

When China began its fixed-investment boom, and later began pumping up its securities markets, global commentators complained that such market interference could not keep growth rates at stellar levels forever.

Such forced investment and market-pumping by a government is a bit like giving athletes strong coffee to speed up their metabolism – the more energy they squeeze out of each muscle cell, the closer they are to running out of energy altogether and potentially falling flat on their face.

That is what is now happening, and the impact on Australian disposable incomes will be as large as it was predictable (as I noted in 2013).

What is alarming is that the boost to incomes projected by the RBA, just last year no less, was set to peak in 2015 and then decline in a fairly benign way.

One of the arguments in favour of that smooth transition was that in iron ore, for example, a huge rise in the volume of exports would offset the deteriorating per-tonne price.

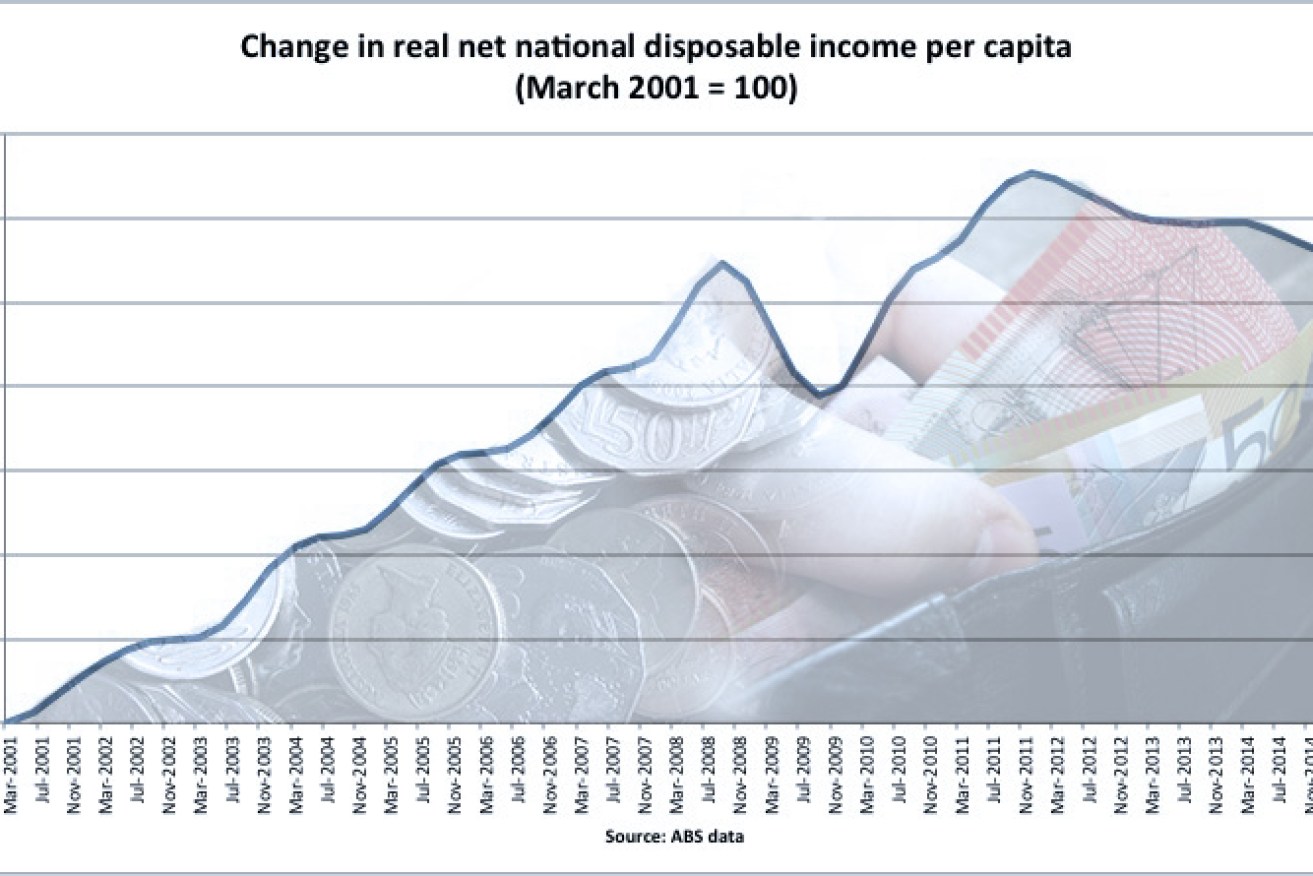

Now if those projections were accurate, even last year, you’d have to ask what the hell was going wrong with the rest of the economy – as the chart below shows, real disposable income per capita has been falling since December 2011.

The truth is that China gave its economic athletes too much coffee.

Its decades-long manufacturing boom, accompanied by currency manipulation to allow the rest of the world to borrow its trade surpluses and buy its goods, worked a treat. That was the first big double-shot latte.

China’s economic athletes have guzzled one too many lattes.

When that plan ran out of puff during the GFC years, the Communist Party replaced global demand and China’s still-weak domestic demand, with a state-mandated fixed-investment splurge. That was like a giant double espresso in a ferro-concrete cup.

That economic miracle lost momentum after producing too many empty buildings and roads to nowhere, so the Chinese government helped create a credit bubble and encouraged individuals to borrow to buy real estate and equities. In recent days it has actually imposed on certain people selling down these assets.

So much for free markets.

The point for Australia, then, is that China’s correction is coming harder and faster than most people expected.

The flow-through effect on disposable income here, as well as for government tax revenues from the resources sector, also look to be greater than expected.

This has been spelled out alarmingly by Goldman Sachs in its most recent note to clients on commodity markets, in which it sees China’s troubles creating a ‘feedback loop’ that will hurt economies such as Australia’s due to the reinforcing role of currency recalibrations.

More articles from Rob Burgess

• Your wage is about to be worth less. Here’s why

• ‘Greek levels’ of debt? No. This is our real debt crisis

• We need to hear the truth about Casino Australia

It notes: “The negative feedback loop is significant. The deflationary impulse created by lower commodity prices reinforces a stronger US dollar, as witnessed by recent moves in FX markets that resulted in weaker commodity currencies.

Our relationship with China has brought cheap cars to Australia, but soon, we may not be able to afford the running costs.

“This decreases the cost of producing commodities in these countries through lower wage costs that are priced in the weaker local currencies.

“Further, this deflationary impulse reinforces a stronger US economy and higher rates. The higher rates in turn raise the cost of funding for emerging markets, which reinforces the need for emerging markets such as China to deleverage and deal with significant macro imbalances developed over the past decade.

“This ultimately reduces the demand for commodities, particularly those that are tied to investment such as copper and iron ore.”

That is not good news for Australia.

That same RBA research quoted above shows that during the boom years, the number one area of expenditure that increased to reflect rising incomes and the strong dollar was the purchase of imported cars.

Chinese stimulus spending gave us a fantastic motor vehicle fleet. The question in the years ahead is whether we’ll be able to afford to run them.

Woolworths faces court over $1m pay bungle

Spend some time to examine cashback details

Apps that help you save on fuel, groceries, time

Fridge, pantry audits vital to cut food waste

Aussies’ mortgage pain hits unwanted high

Jobs market put to test with fresh data due