Ask the Expert: Growth and return – figuring out your individual super progress

Photo: Getty

Question 1

- When the superannuation industry quote their annual growth performance figures, do those figures include employer contributions? The reporting feature of my superannuation account is not transparent to how much private equity has been made when it boasts a net growth figure between given dates.

Performance returns as stated by super funds should be after investment fees and costs and transaction costs.

It should also be less any percentage-based administration fees, but would not take into account a dollar-based admin or membership fee.

As an example, if a fund states it has an 8 per cent return over the past five years, this should be less all fees except any regular admin fee, this is normally only, say, $1.50 per week.

You can check the returns page of your super, which will have a disclaimer that explains all this.

The returns do not include any contributions, tax or withdrawals. That is why everyone’s individual experience will be different as it will be determined by the timing of all these transactions.

Growth of a fund is different to returns. The fund may grow its funds and its administration not just by returns but by adding in new members and existing members switching and adding in new funds.

Speaking of growth and returns, SuperRatings recently released the average 10-year figures for different superannuation investment types.

It assumes $100,000 invested and no further contributions. It uses the average performance of the largest 50 super funds and separates them depending on how many growth assets are contained within the investment.

For example, funds with between 60 per cent and 76 per cent of growth assets are classified as ‘balanced’ as shown below:

Question 2

- I am 70 years old and have an account in each of the pension and accumulation phase in industry funds. Three years ago, my total super balance (TSB) was just over the $1.6 million cap and I stopped all contributions then. My question is, since the TSB limit is now $1.9 million, and my TSB is now much less than that, can I start non-concessional contributions into my accumulation account? Or, does it mean that since my TSB has exceeded the then $1.6 million cap, I can no longer make any further contributions even though the cap is now $1.9 million.

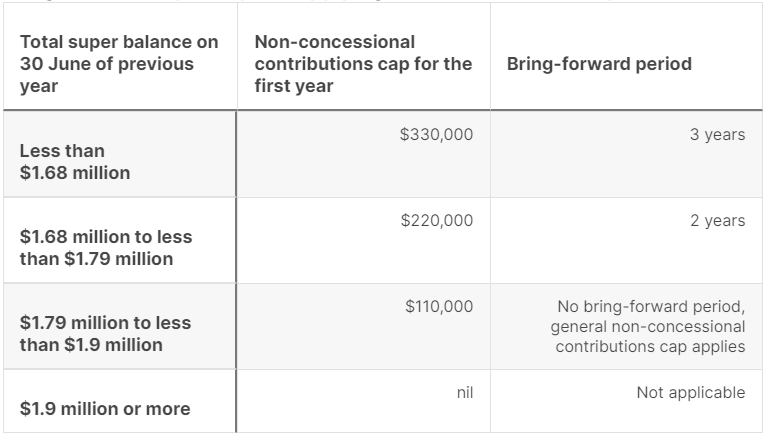

You can look to make further non-concessional (after-tax) contributions to super, regardless of your old super balances.

The only relevant ‘total super balance’ (TSB) figure you need to consider is what it was as at the previous June 30.

So, if your TSB was under $1,900,000 as at June 30, 2023 you are eligible to make non-concessional contributions.

Using the ‘bring forward rule’ you may be able to make non-concessional contributions above the standard $110,000 cap.

This again is dependent on your TSB from the previous June 30 as shown in the below table:

Source: Australian Taxation Office

Question 3

- Age pension was supposed to have a rise – I have not received a rise except for the March one. There is supposed to be another in July but it did not happen. Why?

In July the income and assets test threshold eligibility (how much income and assets you can have) for Centrelink payments are indexed.

However, the payments themselves are only indexed in March and September.

(function(t,e,s,n){var o,a,c;t.SMCX=t.SMCX||[],e.getElementById(n)||(o=e.getElementsByTagName(s),a=o[o.length-1],c=e.createElement(s),c.type=”text/javascript”,c.async=!0,c.id=n,c.src=”https://widget.surveymonkey.com/collect/website/js/tRaiETqnLgj758hTBazgdxSelZMIWnGyT5p0b3bsU27CC8hfyJDoc7jtaUsIUSYm.js”,a.parentNode.insertBefore(c,a))})(window,document,”script”,”smcx-sdk”);

Craig Sankey is a licensed financial adviser and head of Technical Services & Advice Enablement at Industry Fund Services

Disclaimer: The responses provided are general in nature, and while they are prompted by the questions asked, they have been prepared without taking into consideration all your objectives, financial situation or needs.

Before relying on any of the information, please ensure that you consider the appropriateness of the information for your objectives, financial situation or needs. To the extent that it is permitted by law, no responsibility for errors or omissions is accepted by IFS and its representatives.

The New Daily is owned by Industry Super Holdings